Expert Verified

Expert Verified

Contributors:

Quick Summary

- Alternatives to equity release for additional retirement income include renting out, downsizing, using savings, working beyond retirement age, and reevaluating existing mortgages.

- Further strategies to manage finances include extending mortgage terms, reducing expenses such as utility costs, seeking family assistance, exploring new job opportunities, accessing pension funds, and utilising government assistance.

- When considering these alternatives, it is crucial to understand the tax implications of downsizing, the risks associated with renting out a room, eligibility for government programmes, the potential impact of asset liquidation, and the incentives for starting a business venture.

In researching equity release alternatives, it is interesting to find that nearly 1 in 8 retirees in the UK are still paying off their mortgages.1

But did you know that releasing property value is not the only way to unlock your home's value or fund expenses in later life?

Perhaps there is a better solution for you?

In This Article, You Will Discover:

Request a FREE call back discover:

- Who offers the LOWEST rates available on the market.

- Who offers the HIGHEST release amount.

- If you qualify for equity release.

In this review, our expert researchers have found various alternatives to equity release mortgages in the UK such as renting out rooms, downsizing, reevaluating your mortgage strategy, and more.

Read here to find out what alternatives there are.

What Are Equity Release Loans?

Equity release loans are a financial tool for seniors, offering a way to convert the value in their homes into a tangible resource, whether as a lump sum or regular payments.

Read On: How Equity Release Works

What Are the Best Alternatives to Equity Release in the UK?

Downsizing is a top alternative to equity release in the UK.

By selling your larger home and moving into a smaller, less expensive one, you can free up substantial capital.

This solution is particularly viable for empty nesters or those nearing retirement.

Another compelling option is to take in a lodger or participate in a home reversion scheme.

Renting out part of your property can provide a steady income stream, while a home reversion involves selling a portion of your property while still living in it.

Both are practical methods to utilise your property's value without resorting to equity release.

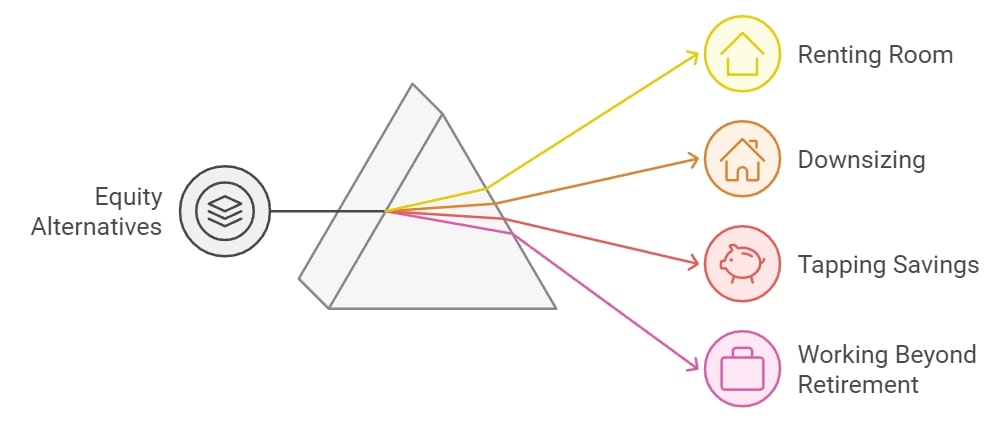

4 Most Common Alternatives to Equity Release

There are many common alternatives to consider apart from equity release loans to raise extra cash.

These include:

- Renting out a room

- Downsizing

- Tapping into your savings

- Working beyond retirement

#1. Renting Out a Room

Transforming an unused room into a source of income has become an increasingly popular move for homeowners.

2 Options to consider:

- Airbnb: You could rent out your spare room by becoming an Airbnb host.2

- Rent a Room Scheme: By utilising this UK Government initiative you could earn up to £7,500 per year, tax-free by renting out your furnished, spare room.3

#2. Downsizing

Downsizing usually happens when families evolve, with children becoming independent or lifestyle preferences changing, a larger property may no longer be necessary or feasible.

Selling your larger property and purchasing a more affordable, smaller one, would enable you to free up extra cash.

Read More: What Martin Lewis Says About Downsizing vs Equity Release

#3. Tapping Into Your Savings

Dipping into your savings can provide immediate financial relief without the hassles of going into debt.

Using your own money from savings accounts or fixed deposits means there are no interest rates, terms and conditions, or repayments to worry about.

Most advisors will probably suggest using savings before releasing equity as this generally does not offer you the full value of your home.

#4. Working Beyond Retirement

Working into retirement means that you can supplement your income without tapping into your current financial reserves.

Since people are generally living longer these days, more seniors today are extending their time in the workforce.4

According to the Office of National Statistics, there had been a huge surge in people over 65 years being employed in 2022.5

12 Other Popular Alternatives

Other popular alternatives could include reducing your expenses or reevaluating your mortgage.

Here is a list of possible alternatives:

- Reevaluate your mortgage

- Managing your financial obligations

- Regularly assessing your expenses

- Liquidating select assets

- Extending your mortgage term

- Reducing utility costs

- Seeking financial assistance from family

- Exploring new job opportunities

- Accessing pension funds

- Planning for retirement income

- Using government assistance

- Starting a business venture

#1. Reevaluating Your Mortgage

By regularly reviewing your mortgage terms, you can assess whether you have the best deal possible.

Consulting with your financial advisor or mortgage broker can give you valuable insight into what mortgage products are available and highlight alternative options to help you save money.

By considering a switch or renegotiating certain aspects of your mortgage, you could potentially enjoy significant savings over the duration of your loan.

#2. Managing Financial Obligations

It is important to effectively manage your financial obligations like your monthly bills, mortgage payments, and credit card debts.

Manage your money by:

- Regularly reviewing your budget

- Have an emergency fund to cover unexpected expenses

- Keeping track of your spending habits

- Avoiding unnecessary debt

#3. Assessing Expenses

Take the time to regularly review and assess your expenses by breaking it down into necessities and luxuries.

This way you can see clearly where your money is going and where to reign in your spending if you need to save money.

#4. Liquidating Select Assets

Asset liquidation refers to converting non-essential valuables into cash.

Non-essential variables could include:

- Tangible assets like jewellery

- Artwork

- Antiques

- Financial assets such as stocks

- Bonds

- Other securities

Bear in mind

Factors such as market demand, the condition and rarity of the item, and current economic conditions can all influence the value and liquidity of assets.

Therefore, seek expert advice before you decide to sell any non-essential assets.

#5. Extending Your Mortgage Term

Extending your mortgage term means that you are increasing the duration of the loan, which spreads out the balance over a more extended period.

This generally means that your monthly mortgage payments will be less, leaving you with more cash each month.

However, there is a notable trade-off.

Even though your monthly payments may be less, the total amount of interest paid over the life of the mortgage may increase, making the overall cost of the loan higher.

#6. Reducing Utility Costs

By reducing your monthly utility bills for electricity, water, and gas you will be able to save money.

Regularly compare the prices of different service providers to make sure you have the best deal for you and switch to another company if necessary.

Also, save by making these simple changes:

- Switch to more energy-efficient LED bulbs

- Use energy-saving appliances

- Add some extra insulation

#7. Seeking Financial Assistance from Family

Seeking financial help from your family is an option to help relieve financial pressure.

By doing this you could possibly benefit from flexible repayment terms, without requiring credit checks or having to endure a lengthy approval process from a formal financial provider.

However

While such arrangements can provide immediate financial relief, it could also strain relationships if terms are not clearly defined or if repayment becomes challenging.

If you choose this route, make sure you clearly document the terms of the agreement to prevent potential misunderstandings or conflicts in future.

#8. Exploring New Job Opportunities

Exploring new job opportunities and procuring new employment can help you to generate additional income if needed.

Therefore if you are still in good health, and want to make sure you have enough savings for your retirement, it makes sense to look for new job opportunities on career portals and other platforms.

#9. Accessing Pension Funds

By accessing your pension funds, you are basically using the contributions that you have saved for this purpose while you were employed.

For many retirees, pension funds are their primary source of income, either withdrawing a lump sum or receiving regular payments from their accumulated pension pot.

Bear in mind.

Most pension funds have rules and age limits in place before withdrawals can be made without incurring penalties, as well as tax implications.

#10. Planning for Retirement Income

Planning for your retirement involves setting up strategies to ensure you have a steady stream of income during your retirement years.

As you transition from a work-based income, having a financial plan in place becomes crucial if you want to maintain your standard of living and expenses.

Many factors, including anticipated retirement age, expected lifespan, desired lifestyle, and potential medical costs, play a role in determining how much you should save for retirement.

#11. Using Government Assistance

In the UK, government assistance programmes are designed to provide support to individuals and families in various areas, from housing and unemployment to health and education.

Whether it is through benefits, grants, or subsidised services, the government has a range of schemes to help senior citizens maintain a certain standard of living.

By staying updated with the latest information, usually accessible through government websites or local council offices, you can ensure you are making the most of the resources available to you.6

#12. Starting a Business Venture

Starting a business could be another option to supplement your income for retirement.

To formalise the venture, individuals must navigate a series of legal and regulatory steps, such as registering the business with Companies House and ensuring compliance with the tax regulator, HM Revenue and Customs (HMRC).

The UK government offers a robust support ecosystem for budding businesses, including various grants, loan schemes, and mentorship programmes, which can aid in the successful launch and growth of new ventures.7

Common Questions

What Are the Alternatives to Equity Release

What Are the Tax Implications Associated with Downsizing My Property

What Are the Potential Risks of Renting Out a Room in My Home, and How Can I Mitigate Them

What Are the Specific Eligibility Criteria for Government Assistance Programmes in the UK

How Can I Determine the Fair Market Value of My Assets Before Considering Liquidation

What Are the Top Industries or Sectors Currently Offering New Job Opportunities for Retirees

Are There Any Grants or Financial Incentives Available for Starting a Business Venture in the UK

Conclusion

From downsizing and renting out rooms to reevaluating mortgages and exploring new job opportunities, the UK offers a range of options tailored to individual circumstances and needs.

The right decision for you would depend on your personal preference, long-term goals, and current financial standing.

When considering alternatives to equity release, it is best to seek advice from a qualified financial advisor to help you make a choice that would align with your unique situation.