Equity Release Criteria (2026) Are You Missing Out?

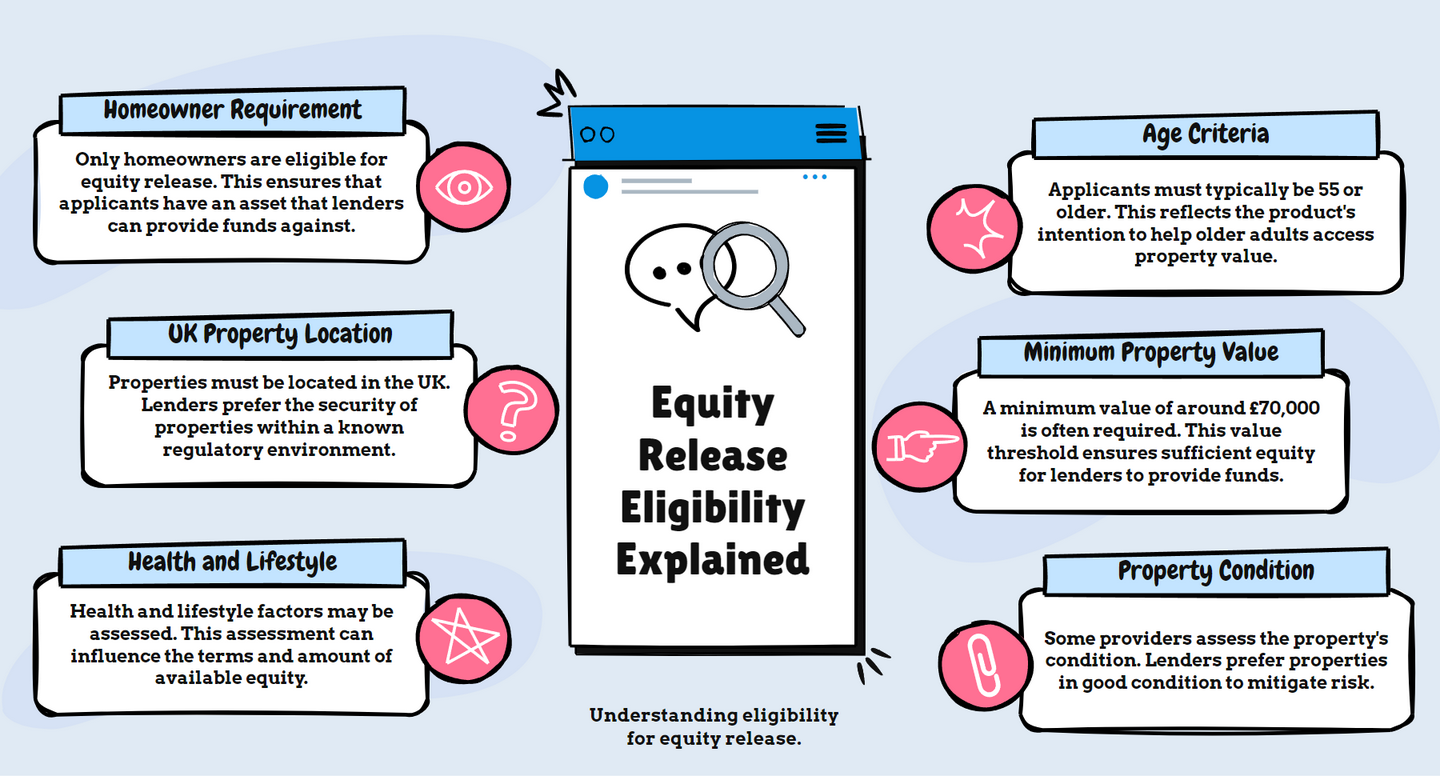

Criteria for equity release typically include being over a certain age (usually 55 or older), owning a home in the UK, and having a property of a certain minimum value.

This article contains tops tips from our experts, backed by in-depth research.

Katherine Read is a Financial Writer Known for Her Work on Financial Planning and Retirement Finance, Covering Equity Release, Lifetime Mortgages, Home Reversion, Retirement Planning, SIPPs, Pension Drawdown, and Interest-Only Mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

Paul Is an External Compliance Expert and the Director of Alpha Capital Compliance Limited, Known for Its No-Nonsense Approach to Financial Compliance.

Paul Is an External Compliance Expert and the Director of Alpha Capital Compliance Limited, Known for Its No-Nonsense Approach to Financial Compliance.

Last Updated: 11 Mar 2025

Key Takeaways

Eligibility for equity release generally requires homeowners to be at least 55 years old and own a property in the UK that meets certain standards and value thresholds typically set by lenders.

Age plays a crucial role in the terms offered for equity release, with older homeowners often receiving more favourable terms due to the shorter expected duration of the loan.

While standard construction homes and flats are usually eligible for equity release, properties with non-standard features such as thatched roofs or timber frames may be excluded.

Equity Release Criteria may sound daunting, but consider this: the average homeowner was able to release just over £106,000 of equity in 2022.1

As leading researchers in UK finance, we are here to guide you through the ins and outs of who qualifies for such financial products.

In This Article, You Will Discover:

Who Offers the Lowest Equity Release Rates in 2025?

Request a FREE call back discover:

Who offers the LOWEST rates available on the market.

To maximise the value of your property and give you a more secure financial future, you must fully understand these criteria.

This article is packed with practical advice and valuable takeaways, answering all your questions on the basic requirements, age limits, property values, and more.

Let us dive in…

Explain Equity Release

Equity release explained: Equity release is a financial solution tailored for older homeowners, enabling them to benefit from the value of their property without sacrificing their living arrangements.

What Are the Eligibility Criteria for Equity Release in the UK?

In the UK, the eligibility for equity release largely hinges on age, property value, and property type.

Typically, homeowners must be at least 55 years old, though some providers stipulate a minimum age of 60.

The property must be your primary residence and be worth a minimum of £70,000, although this threshold may vary depending on the equity release provider.

Certain property types may not qualify for equity release.

For instance, freehold flats and maisonettes usually aren't accepted.

The property should be in good condition, and any existing mortgage must be paid off with the proceeds from the equity release.

It’s crucial to note that eligibility requirements might differ among providers, so it's always imperative to check with multiple sources before making a decision.

What are the Basic Requirements for Equity Release?

With a lifetime mortgage, the most popular of these products, the basic requirements include being at least 55 years old, owning a property of a certain value, and being your main residence.

Is There an Age Criteria to Qualify for Equity Release?

Yes, there are age criteria and the minimum age is usually 55 with a lifetime mortgage or 65 with a home reversion scheme.

If you and your partner have joint property and opt for equity release, you must be of the minimum age to qualify.

There is no legal upper age limit, although some providers may have an age cap, and the amount you can borrow generally increases with age.

How Much Can I Borrow Against My Home?

The amount you can borrow, known as the loan-to-value (LTV) ratio, is typically between 20-60% of your property's value.2

However, this depends on factors such as your age and health.

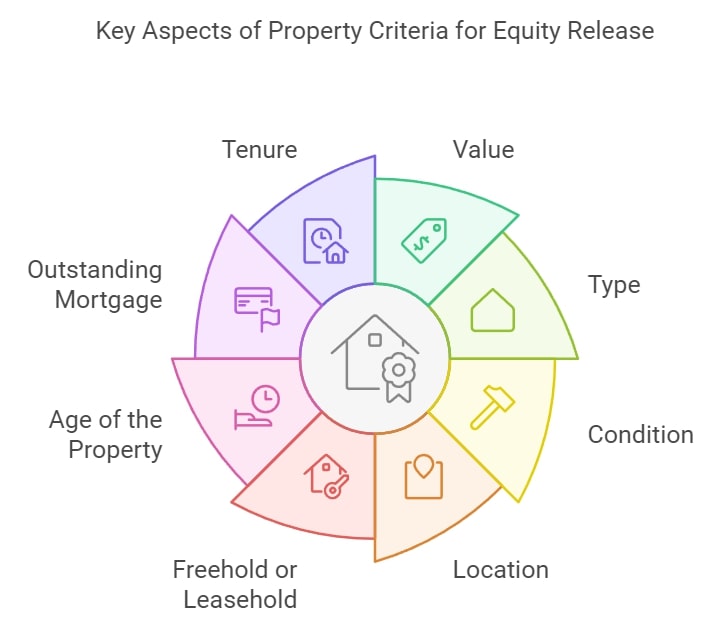

Key Aspects of Property Criteria for Equity Release

Understanding the key aspects of property criteria is essential for homeowners considering this financial option.

The following are the most important aspects:

Value: Your home must usually be worth at least £70,000, but the amount is lender-dependent.

Type: Standard property types such as detached, semi-detached, terraced houses, and bungalows are generally eligible. Some providers may have restrictions on flats, particularly if they are ex-council.

Condition: The property should be in good structural and cosmetic condition. Necessary repairs or structural issues can affect eligibility or the amount available for release.

Location: Your home must be in the UK, but some lenders restrict certain regions or postcodes.

Freehold or Leasehold: Freehold properties are typically accepted. Leasehold properties are usually accepted if the lease has a significant period remaining, often 80-90 years at a minimum.

Age of the Property: Older properties may be subject to additional scrutiny to ensure they meet modern standards. Some very historic or listed buildings may have restrictions.

Outstanding Mortgage: An outstanding mortgage or secured loan on the property must typically be paid off before or by using the proceeds from your property equity.

Tenure: Ensure that no other 3rd parties have rights over the property that could affect qualification.

Unique Properties: Unconventional properties, such as those made of non-standard materials or unique architectural features, may be subject to additional evaluation or not qualify.

Future Saleability: Providers consider the future saleability of the property, ensuring they can recover their funds since it is a loan secured against the home.

Each provider has different criteria, so this is just a basic overview.

Anyone considering releasing property value must seek expert advice to understand the implications and criteria specific to their circumstances and chosen provider.

What is the eligibility criteria for equity release in the UK

The eligibility criteria for equity release in the UK typically include being at least 55 or 60 years old, depending on the provider, and owning a property that is worth a certain minimum value.

Other factors that may be considered include the outstanding mortgage on the property, the location of the property, and the overall health and lifestyle of the applicant.

It is important to note that each provider may have slightly different eligibility criteria, so it is essential to research and compare different options before making a decision.

How does age affect equity release criteria

Age plays a significant role in equity release criteria.

Generally, the minimum age requirement to be eligible for equity release is 55 or 60, depending on the provider.

The older you are, the higher the percentage of your home’s value you can release.

This is because the provider assumes a shorter repayment period due to life expectancy.

Older individuals may also have a higher chance of qualifying for enhanced plans that offer more favorable terms.

However, it is essential to carefully consider the potential impact on inheritance and seek professional advice to make an informed decision.

What are the property requirements for Equity release

The property requirements for Equity release typically include owning a property in the UK that is your primary residence.

The property should be of standard construction and in good condition, meeting the provider’s valuation criteria.

Leasehold properties may also be eligible, but the lease must have a certain minimum term remaining.

It is also important to note that some providers have specific restrictions on property types, such as flats in certain locations.

Consulting with a qualified equity release adviser can help determine if your property meets the requirements of different providers.

Can I Use Equity Release If I Have a Mortgage

It is possible to use equity release if you have a mortgage.

However, the outstanding mortgage balance will need to be repaid first from the funds released through equity release.

This can be done by either using some of the released funds or by combining the mortgage and equity release into a new product.

It is crucial to consider the potential impact on your financial situation and seek professional advice to understand the best course of action based on your individual circumstances.

What are the risks and benefits of meeting equity release criteria

Meeting equity release criteria can offer both risks and benefits.

The main benefit is the ability to access a tax-free lump sum or regular income while remaining in your home.

This can help supplement retirement income or fund specific expenses.

However, it is important to be aware of the risks, such as the potential reduction in inheritance, the impact on means-tested benefits, and the potential for compounding interest over time.

Seeking independent advice from a qualified equity release adviser can help you understand the potential risks and benefits in detail and make an informed decision.

What Does It Mean to Release Equity on a Freehold Property

Releasing equity on a freehold property means you can access your home’s ‘locked’ value while still retaining ownership of it.

Can I Release Equity on a Leasehold Property

Yes, releasing equity on a leasehold property is possible if the lease has at least 75-80 years remaining.3

The lease term is vital as it ensures that the property retains value over the plan’s duration.

To determine loan risk, lenders assess the lease’s unexpired term and other conditions.

A shorter lease may undermine the lender’s security, making the property’s age, location, and lease terms crucial to the decision.

Consulting with a financial advisor or specialist will be necessary to navigate this complex process.

Is Equity Release Possible on Commercial or Business Properties

Yes some lenders may offer schemes for commercial or business properties, even though they are primarily for residential properties.

It is crucial to consult with financial experts familiar with commercial transactions before proceeding.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

I think you’ll agree with me when I say that it’s REALLY hard to choose the best ABC with all the choices available.

After hundreds of hours of testing and reviewing, we have strong opinions about what makes the best ABC.

We highlight the pros, cons and features of the ABC.

How Can Equity Release and Power of Attorney Work Together

If a homeowner has appointed a Power of Attorney (POA), the POA can make decisions regarding equity release.

However

They must act in the homeowner’s best interests, and lenders may require specific legal documentation and request additional safeguards.

Conclusion

Equity release can give you financial security and independence if you are over 55 years old, but it also has some risks, such as lowering the value of your estate, possibly making it harder for you to obtain financial help, and possibly having to pay extra fees if you pay off the loan early.

A thorough understanding of these criteria can lead to more informed decisions regarding whether or not to proceed with such a financial agreement, and the need for individualised guidance underpins every decision.

Equity release is as unique as the people considering it, so if you are considering using your home to boost your finances, you should review the equity release criteria to see if it is right for you.

Expert Verified

Expert Verified